3Q4F

Quantum Reinformcemnt Learning based Financial Stock Trading using Technical Indicators.

Created on 11th February 2024

•

3Q4F

Quantum Reinformcemnt Learning based Financial Stock Trading using Technical Indicators.

The problem 3Q4F solves

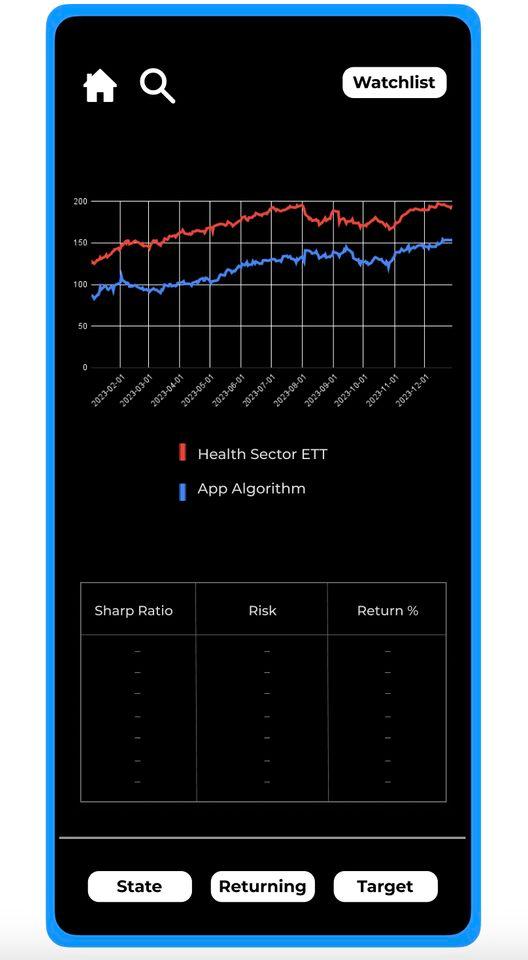

Providing a Reinforcement Learning Based Trader that has sound performance, faster convergence, and better balance of exploration and exploitation to cover all sorts of strategies in a dynamic market environment.

Challenges we ran into

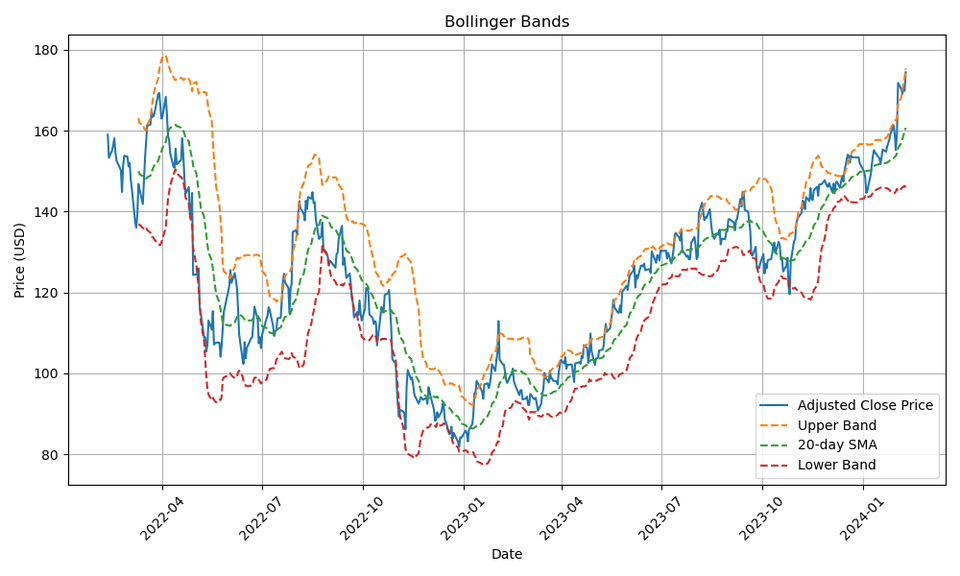

- In implementing Markowitz's modern portfolio theory, our strategy involved rigorous analysis of historical returns, correlations, and volatilities of individual stocks within the portfolio. By dynamically adjusting asset allocations based on changing market conditions, we aimed to maintain an optimal balance between risk and return. This approach enabled us to capitalize on opportunities for alpha generation while systematically mitigating downside risk, thereby enhancing the portfolio's risk-adjusted returns over time.

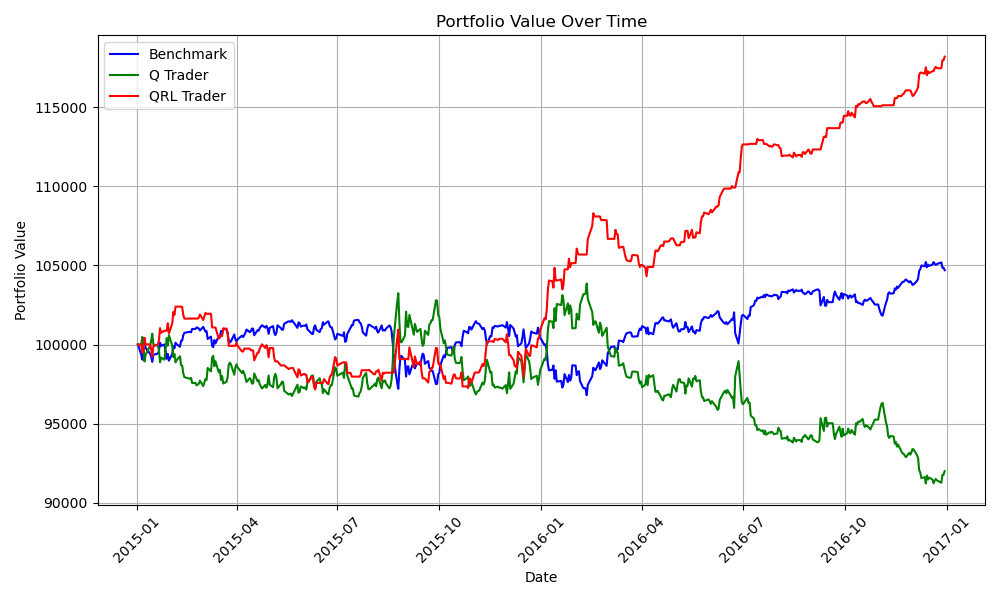

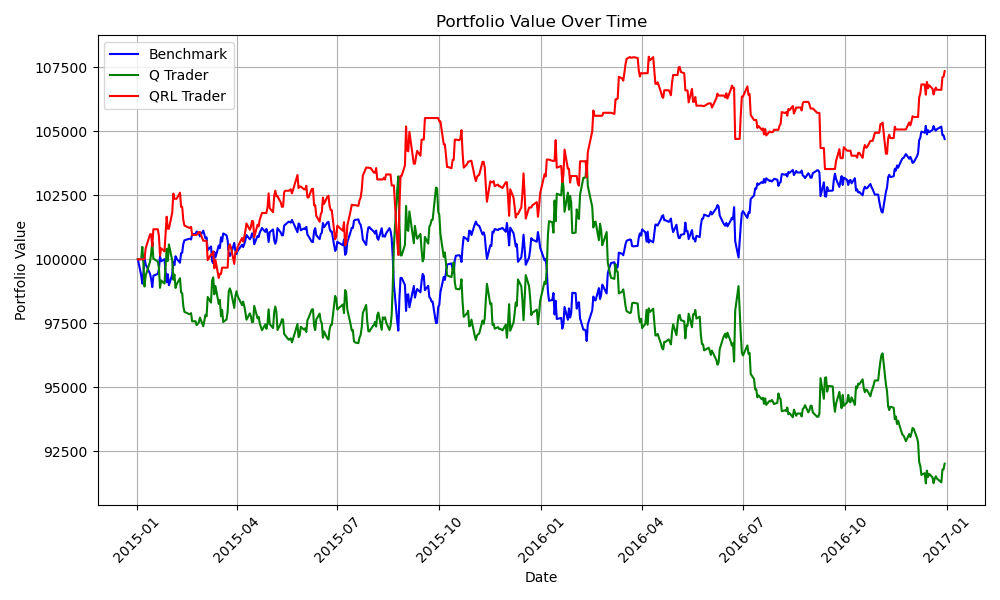

- As the quantum computing-based portfolio optimizer continues its operation, it may generate significant fluctuations in asset allocation, resulting in the execution of substantial trade volumes. This heightened trading activity could precipitate adverse market impact, particularly pronounced for less liquid assets or during periods of heightened volatility. To preemptively address such challenges, the implementation of transaction costs emerges as a prudent measure. Additionally, the imposition of constraints on portfolio turnover serves as a strategic mechanism to mitigate the frequency and scale of allocation adjustments. These interventions not only mitigate the risk of excessive trading costs but also promote stability in portfolio management practices, thereby enhancing overall investment efficacy

Tracks Applied (1)

Finance

Discussion

Builders also viewed

See more projects on Devfolio