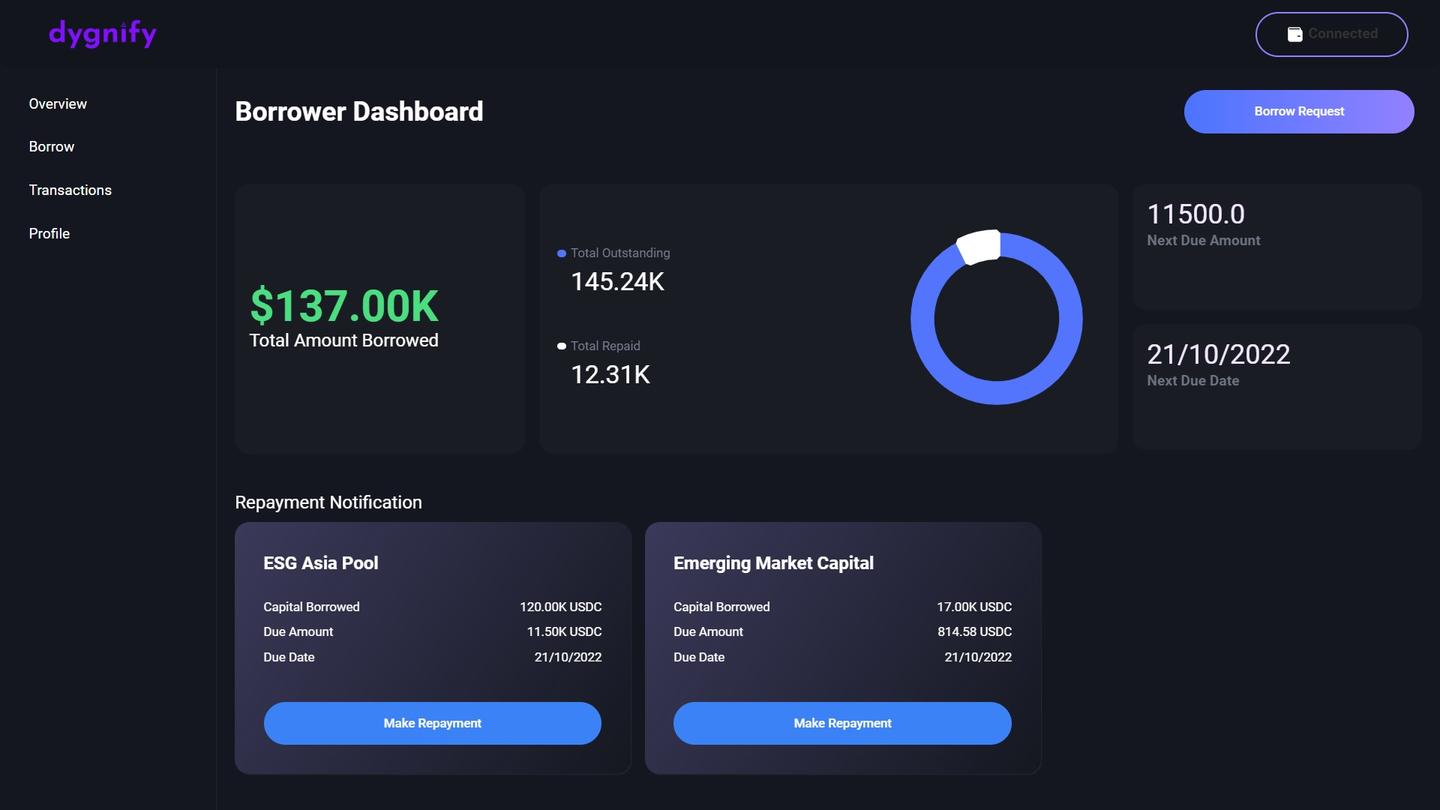

Defi protocol for lending to real world businesses

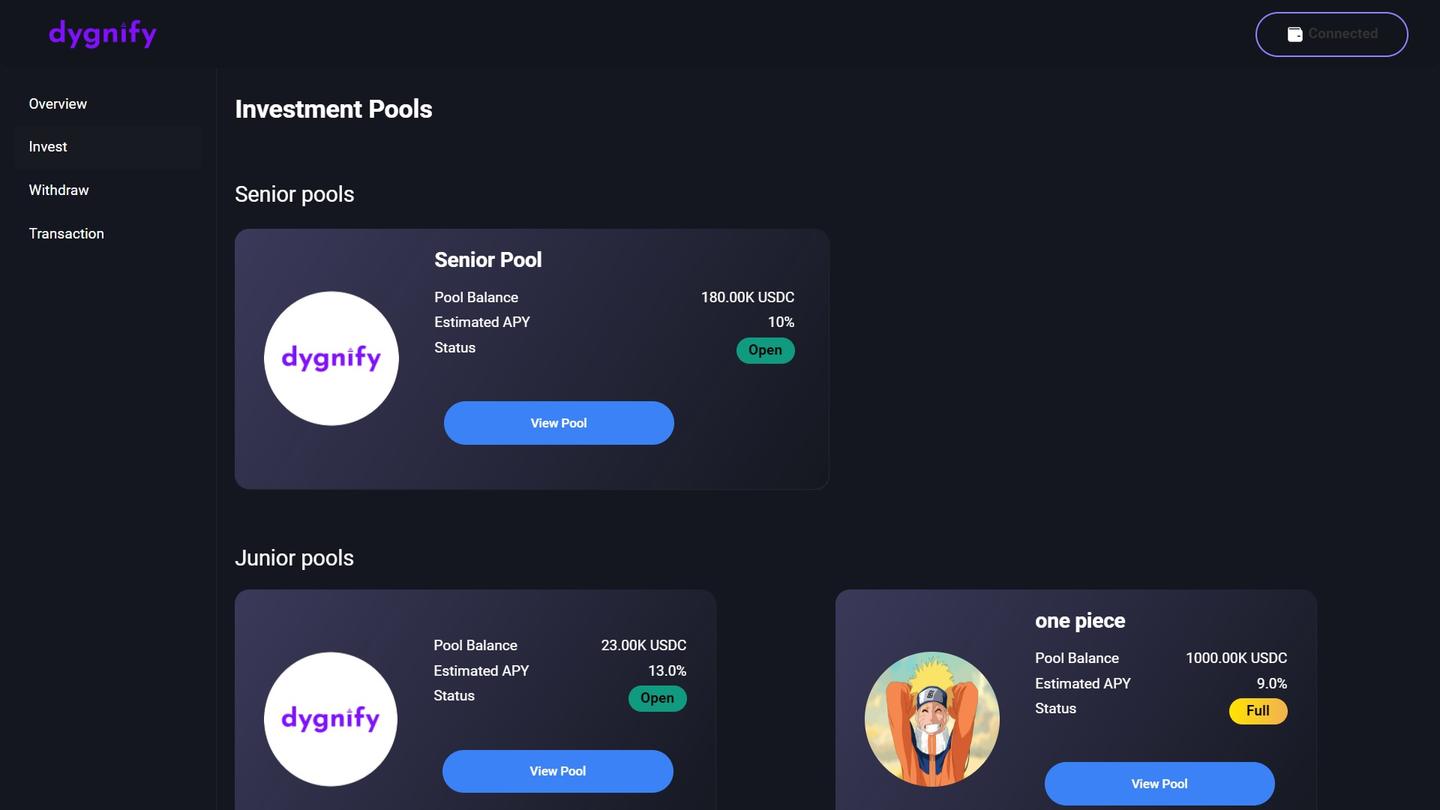

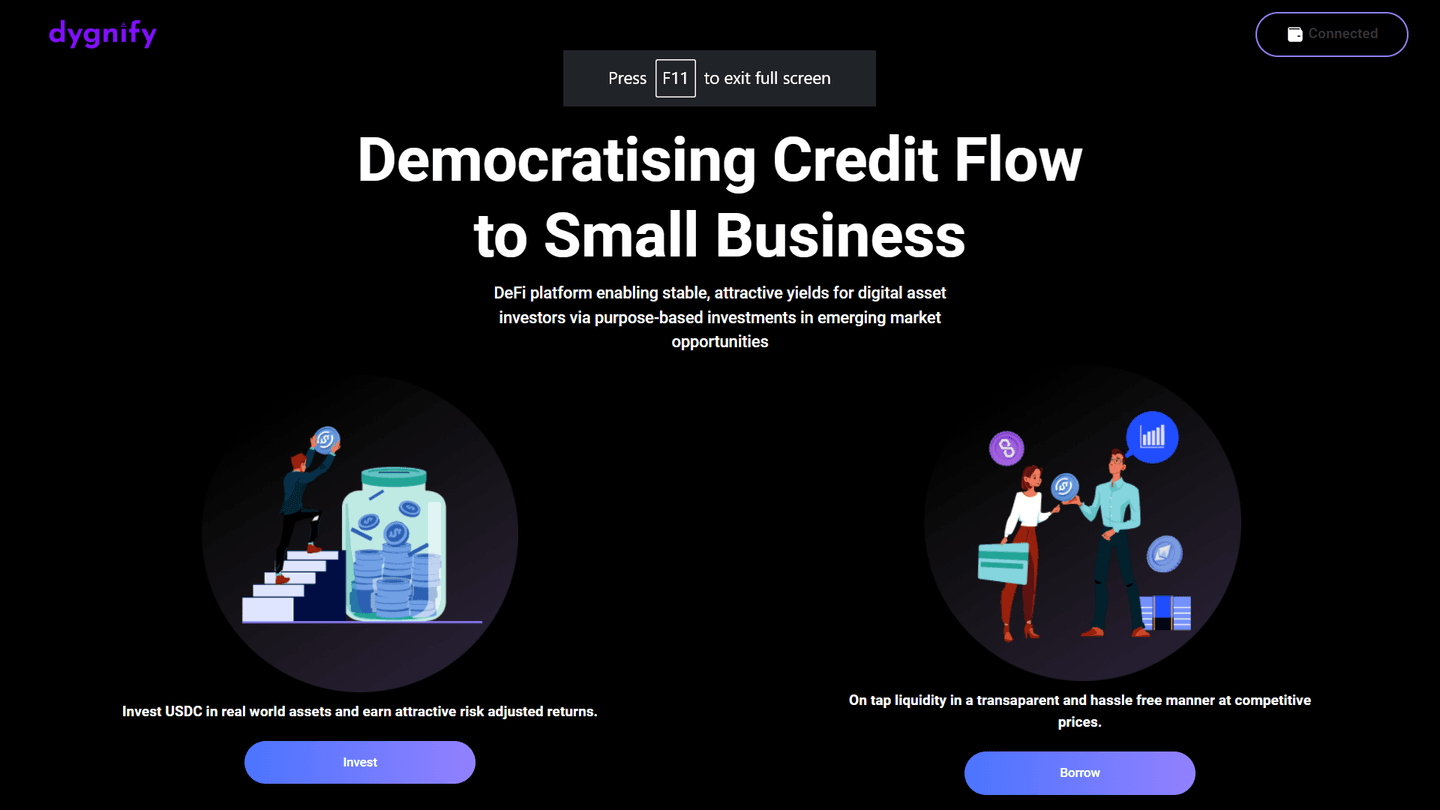

Decentralised credit infrastructure for connecting digital asset investors to invest, as per their risk appetite, in opportunities linked to SMB economic activity, ensuring stable & sustainable yields

Created on 27th August 2022

•

Defi protocol for lending to real world businesses

Decentralised credit infrastructure for connecting digital asset investors to invest, as per their risk appetite, in opportunities linked to SMB economic activity, ensuring stable & sustainable yields

The problem Defi protocol for lending to real world businesses solves

Inspiration for Dygnify comes from our interaction with hundreds of small businesses (“SMB”) who fail to access formal financing and spiral into the debt trap. Our project is a means to enable financial inclusion at scale, enabling SMBs to build a transparent on-chain credit track record so that they can access global pools of capital at affordable cost. Enabling larger capital pools to flow to the SMB funding chain, will ensure better access to credit to SMBs. We plan to build the protocol as an infrastructure toolkit to serve fololwing key purposes:

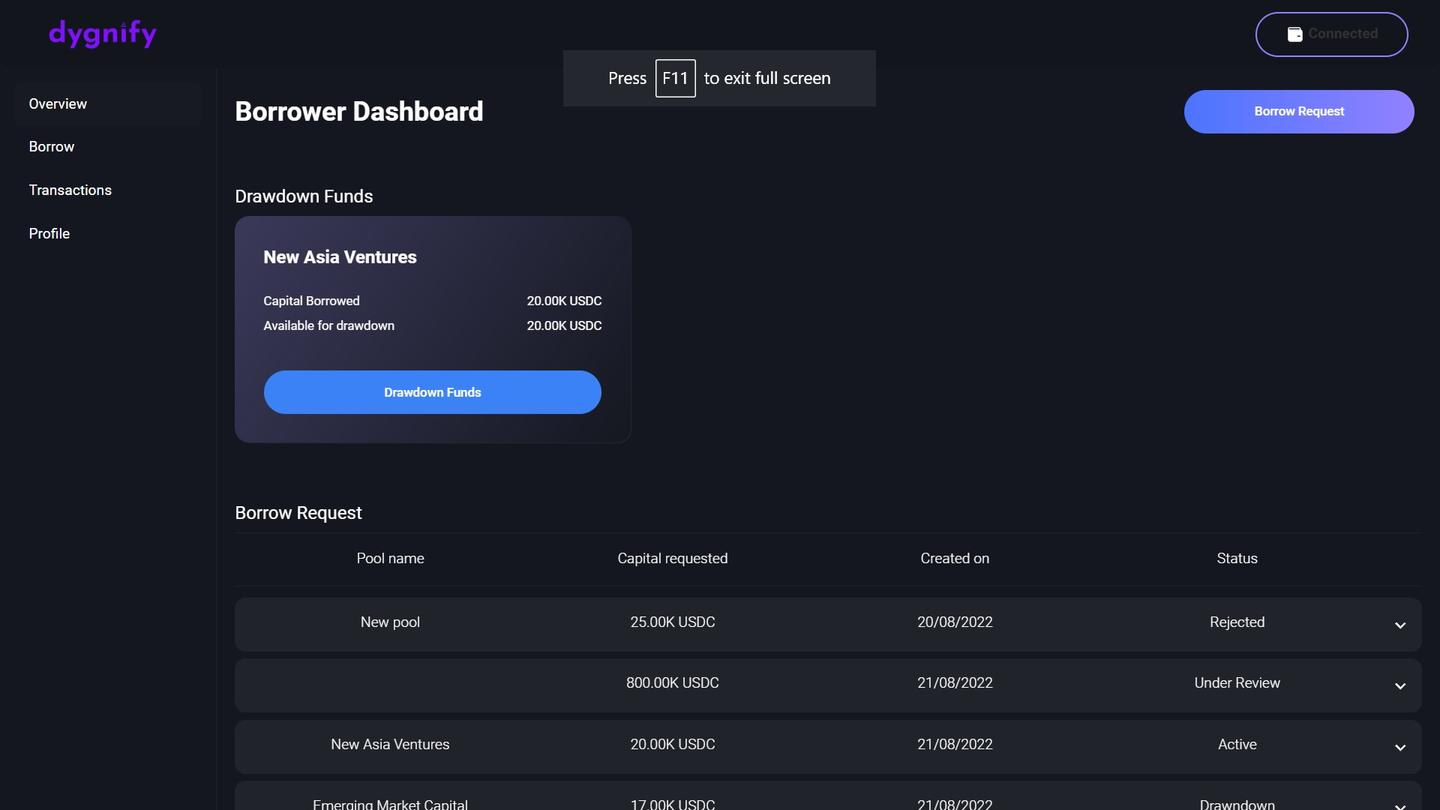

a. Creating an end-to-end workflow connecting Digital Asset Investors with Real World Lending Businesses focussed on lending to Small Businesses

a. Taking away crypto and DeFi complexity for users

b. Providing on+off chain reputation & identity management, regulatory compliance

c. Enabling Security and Privacy Example – tools for on+off chain credit scoring, Reputation management, whitelisting, compliance, decentralised data storage, dash boards etc. with encryption and security features built-in.

Our protocol helps solve the financial inclusion problem sustainably by bringing the following benefits:

-

For the borrowers:

a. Tapping global digital asset liquidity bringing sustainable lower-cost solution for emerging market borrowers

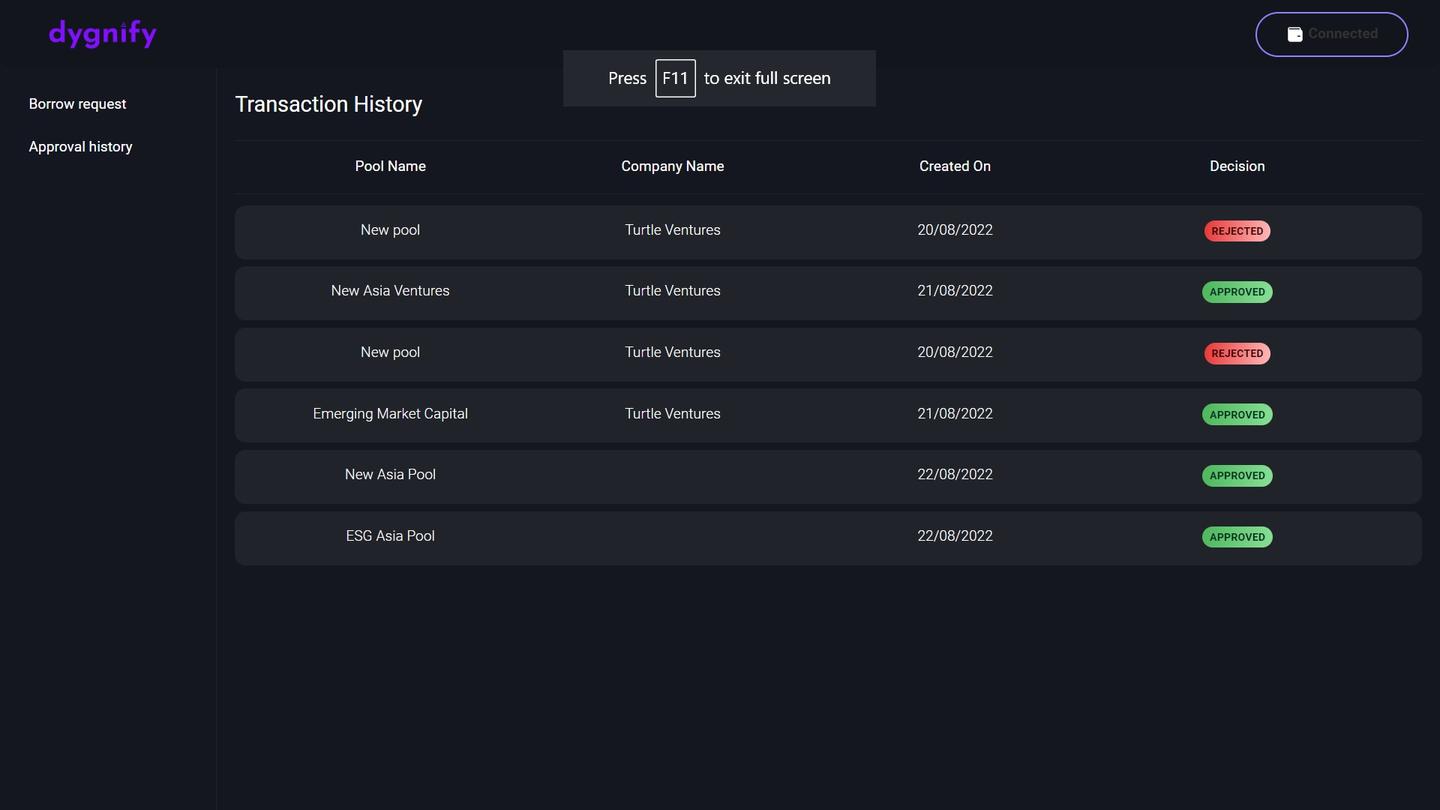

b. Accessing Blockchain based on-chain borrowing, which is fast, secure and creates an immutable credit track record which can open the flood gates to capital -

For the investors:

a. Empowering any digital asset holder to become a lender, backing real-world economic activity

b. Stable, sustainable yields delinked from crypto volatility

We plan to progressively decentralised the protocol by building a community (DAO) of underwriters, auditors, service providers, asset originators, developers and investors; with an incentive mechanism designed to yield good behaviour, can solve for centralised decisioning across the network.

Challenges we ran into

- Internal Integration testing across investor and borrower modules – multiple scenarios and inter-dependencies took a lot of time and thinking to get right.

- Hosting our Dapp on decentralized hosting platform Spheron. Worked collaboratively to stitch all integrations that are working well now.

- Deciding a meaningful chunk of functionality to implement during Unfold2022 Hackathon, given that this was a continuing piece of work. As a team we huddled together and decided to complete the final leg along with computations of yield - most critical element for Defi investors to be completed during this Hackathon. Hence we built and completed this final module + made edits to the previous modules to make them a bit more polished.

Cheer Project

Cheering for a project means supporting a project you like with as little as 0.0025 ETH. Right now, you can Cheer using ETH on Arbitrum, Optimism and Base.