Defi Credence

Redefining Defi, by bringing credit score on-chain

Created on 10th December 2023

•

Defi Credence

Redefining Defi, by bringing credit score on-chain

The problem Defi Credence solves

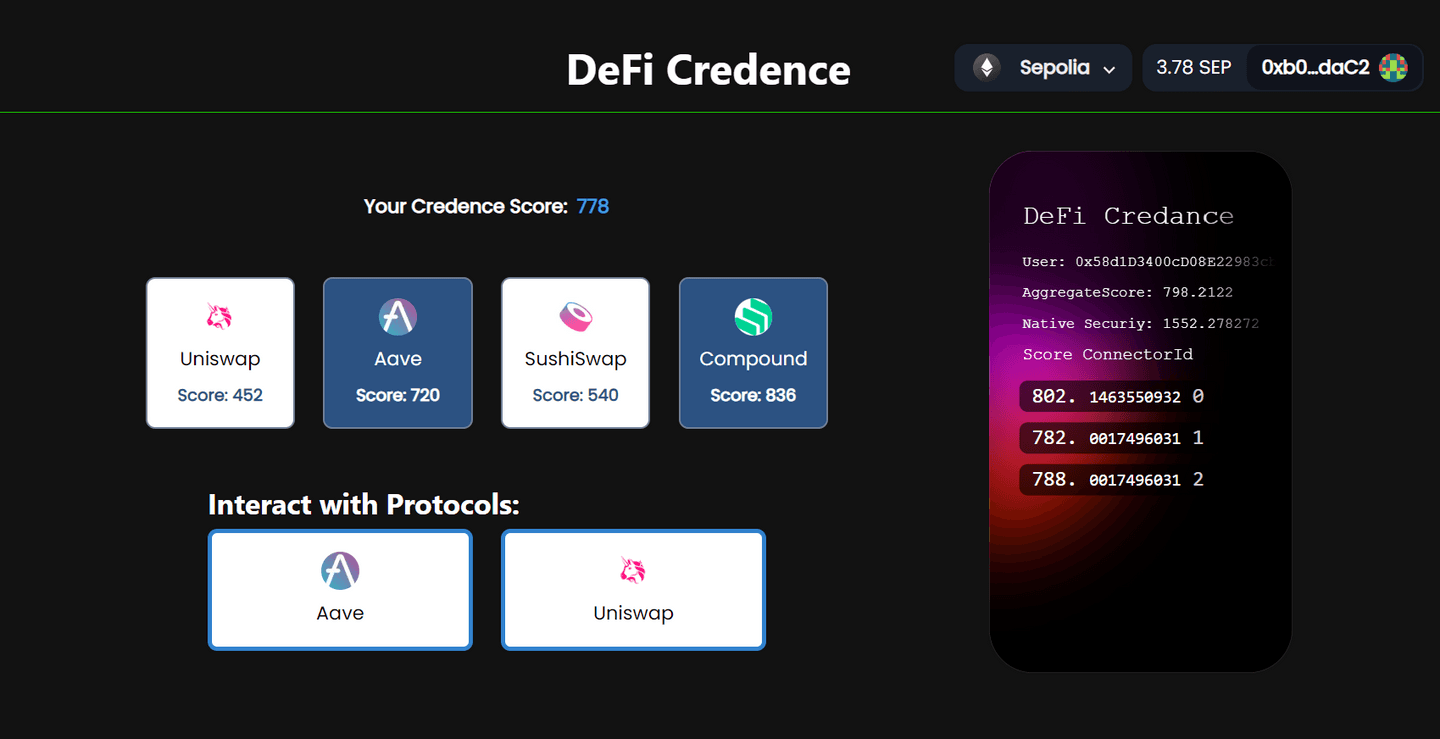

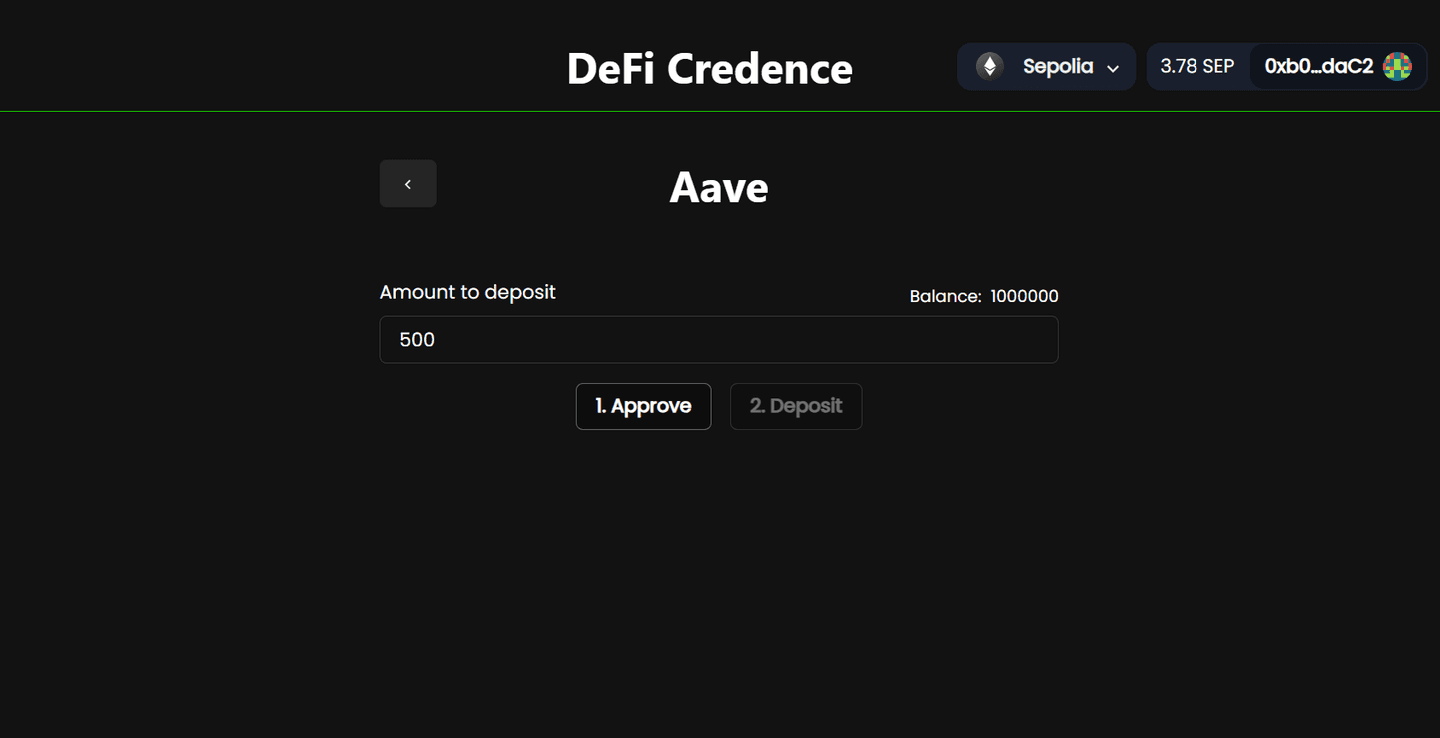

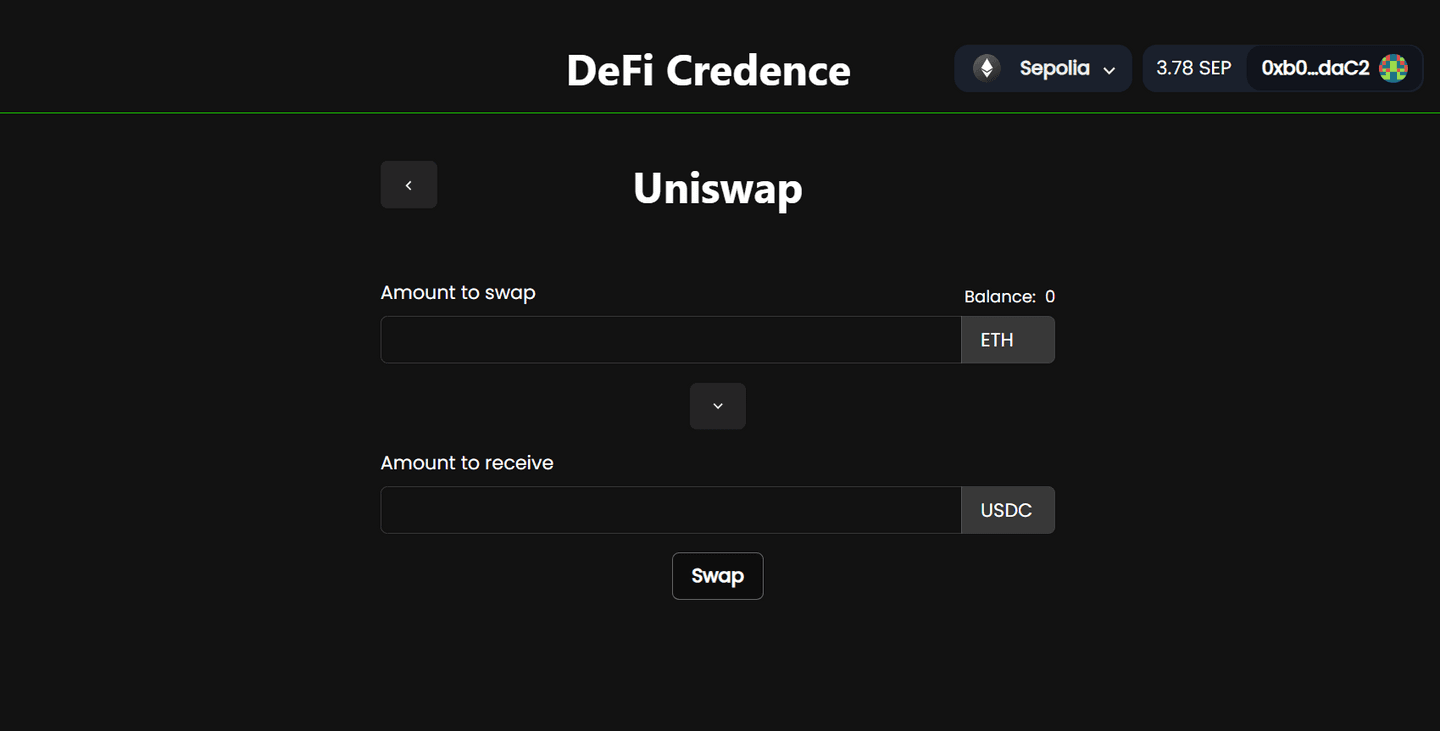

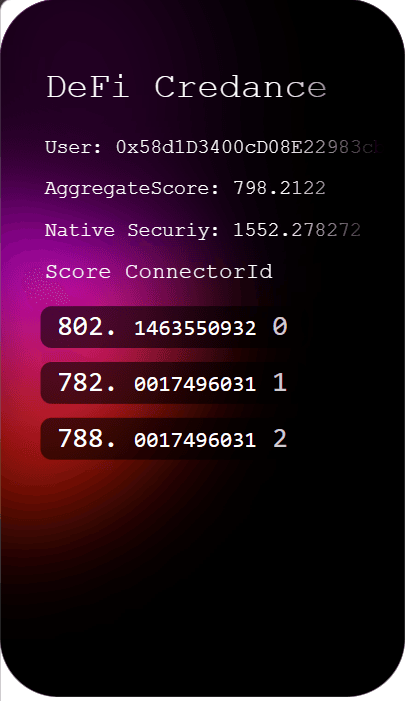

Today most of the financial decisions in defi are a result of greed. For instance, paying back a loan on Aave is equivalent to paying back a friend, it's up to the user, for you to liquidate, and that doesn't negatively impact your access to defi in any way. We tried to solve this problem but building Defi Credence. When it comes to Defi, the problem is how each protocol, affects your score based on your actions, on-the-go. Since there can be a lot of unique protocols, the best way is to have a separate mechanism for each. As a result, Defi credence uses a system called "Connectors" which are protocol specific, and forked protocols can simply be subscribed to with the connector's owner's permission. Note that any number of connectors can be deployed, hence making connectors "ownable" doesn't affect the decentralization of the protocol. The core module operates in a permissionless environment and can be used to aggregate different connectors. For eg. I am a service that wants to know the data related to a user when it comes to lending markets only. So I can use Aave and compound's connector and aggregate the result that is relevant to my need ( under-collateralised loans ).

Some use cases:

- Similar to wealth managers, we assess user's risk profile, based on their activities, aiding in making better financial decision making.

- Web3 login: tailored experience on decentralised apps.

- Credit staking: building financial reputation.

- Protocol design: lower collateral requirements and better products.

- Customised lending loans.

Connectors also give proprietorship companies ( like experian ) to also have a cibil score maintained on-chain.

Challenges we ran into

- Understanding zk primitives and how to make "private" connectors. Thanks to stackr the complexity of proving state was taken away and helped us get over the given blocker.

Tracks Applied (7)

Arbitrum Track

Arbitrum

Celo Track

Celo

Airstack Track

Airstack

Base Track

Base

Mantle Network Track

Mantle Network

OKX Track

OKX

Scroll Track

Scroll