Buck

Money is simple. Buck makes it easy.

Created on 31st July 2020

•

Buck

Money is simple. Buck makes it easy.

The problem Buck solves

Context - Every single working professional (not born into wealth) in the large Indian middle-class is unified by one aim - to get to a state where they no longer need to work for money. In the same context, Warren Buffet famously said - "If you don’t find a way to make money while you sleep, you will work until you die". Without getting into too many statistics many Indians don't do that. In fact, Indian millennial investment rates are among the lowest in the World. Why?

Problem - As Daniel Kahneman says we humans are predictably irrational. We cannot match what we want with how we spend our money. We cannot value optionality. We are swayed by emotions and fear. We overvalue losses (endowment effect) when compared to gains. In short, we have biases that come in the way of making good decisions. Buck solves for those biases.

What is the not the problem - Complexity of Finance is not a problem we solve for. We believe Finance is simple. Morgan Housel, one of the most respected economists alive has a portfolio of 1 index fund and 2 stocks. This approach will work for 90% of individuals. Although sticking to this approach, while simple is not easy. Our job is to make it easy for the user.

Solution - Since human biases are predictable, we leverage those biases using techniques from behavioral finance to guide the user to making and sticking to good financial decisions. Using AA, we obtain the financial history of a consumer and run our proprietary behavioral finance algorithm on it. The experience for every user will be different depending on what we learn about them from their history. We use loss aversion bias to get people to save more/ invest better. We make financial independence a very tangible goal and use gamification and goal-setting theory to get the users to make good investing decisions. We highlight the opportunity costs to make the impact of decisions real. Design principles and technology along with behavioral finance underpin everything we do.

Challenges we ran into

The two biggest challenges we ran into were:

Solving for biases - How does one build something which removes biases which are inherent was a question that we grappled with. For instance, a user who overspends every month has a short term bias i.e he/she overvalues the short term and undervalues the long term. While we can show charts and numbers showing they overspend, it is unlikely that will change their behavior. After a lot of brainstorming, we reframed our problem from "removing biases" to "negating the ill effects of biases". That opened our minds to come up with the solution of leveraging irrational behavior for the good of the user. In the previous instance, we can leverage "loss-aversion" bias, showing how much a user "lost" because of his/her spending patterns to help them change.

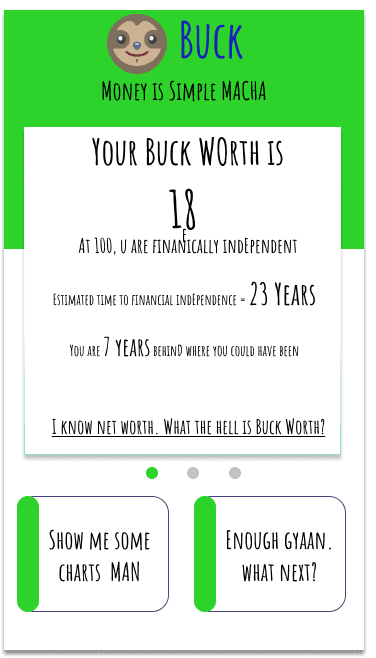

The inherent subjectivity in personal finance - "Personal finance", as the name indicates is subjective. Every individual is different and everyone has different goals and wants. That is exactly what makes it a hard problem. We wanted to build a solution that helps negate the ill effects of bias on a user - while we want it to be customized, at its core it should offer every user something novel while addressing a universal need. Only then it will stand out among all the other apps in the market. We spoke to a lot of users to figure out their thinking around it and realized that the common thread that binds most users is the goal of "financial independence". Every user mentioned this as their goal but no one really understands what it means. That's when we came up with the Buck score - a proprietary score to measure the progress of a user on their journey toward financial independence. The Buck score not only addresses a universal need of users but also serves as a dynamic and tangible progress bar that shows the users the impact of their financial decisions in near real-time - all of this by leveraging the AA framework.

Technologies used